Compare Usage-Based Car Insurance: Rates, Discounts, & Requirements [2024]

Usage-based car insurance uses a device in your car to more accurately track when and how you drive. Enrolling could save you up to 30% on your monthly rates.

Free Car Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Brandon Frady

Licensed Insurance Agent

Brandon Frady has been a licensed insurance agent and insurance office manager since 2018. He has experience in ventures from retail to finance, working positions from cashier to management, but it wasn’t until Brandon started working in the insurance industry that he truly felt at home in his career. In his day-to-day interactions, he aims to live out his business philosophy in how he treats hi...

Licensed Insurance Agent

UPDATED: Nov 7, 2023

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident car insurance decisions. Comparison shopping should be easy. We are not affiliated with any one car insurance company and cannot guarantee quotes from any single company.

Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from top car companies please enter your ZIP code above to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.

UPDATED: Nov 7, 2023

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident car insurance decisions. Comparison shopping should be easy. We are not affiliated with any one car insurance company and cannot guarantee quotes from any single company.

Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from top car companies please enter your ZIP code above to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

| USAGE-BASED INSURANCE | STATISTIC |

|---|---|

| Number of Users | Around 12 Million |

| Estimated Average Savings | Up to 30% |

| Participating Companies | Allstate, American Family, Farmers, Geico, Liberty Mutual, Nationwide, Progressive, State Farm, Travelers, USAA |

Usage-based insurance is a quickly growing segment of the car insurance market. But many folks don’t know what it is or how it works.

That’s why we’ve created this guide: to help you understand the basics of usage-based insurance, which is similar to pay-per-mile auto insurance, and see if it’s the right fit for you and your family. Get started on your car insurance journey today by entering your ZIP code, and read on to find more about usage-based coverage.

What is usage-based car insurance?

According to Washington State’s Office of the Insurance Commissioner, “Usage-based insurance (UBI), also called ‘telematics,’ is when an auto insurer monitors and tracks your driving behavior through a device installed in your vehicle or through a smartphone application. These wireless devices transmit data in real time back to insurers, such as:

- Number of miles you drive

- Time of day

- Where you drive the vehicle

- If you rapidly accelerate, rapidly decelerate and/or take corners hard

- Your air bag deploys”

In the sections below, we’ll cover the basics of what you need to know about usage-based car insurance.

Average Savings by State for UBI Programs

What we’ve done is average the typical savings for UBI programs based on the companies we researched below. That number was 29 percent. We then looked at NAIC rate data by state and deducted the 29% for each state. That will give you baseline as you’re researching which UBI may be right for you.

| STATE | Potential Savings with UBI from Average | Average | 2015 | 2014 | 2013 | 2012 | 2011 |

|---|---|---|---|---|---|---|---|

| Alabama | $580.75 | $817.95 | $868.48 | $837.09 | $811.75 | $788.07 | $784.38 |

| Alaska | $744.51 | $1,048.60 | $1,027.75 | $1,050.09 | $1,058.15 | $1,053.54 | $1,053.48 |

| Arizona | $661.79 | $932.10 | $972.85 | $961.88 | $926.52 | $899.91 | $899.33 |

| Arkansas | $617.25 | $869.37 | $906.34 | $900.18 | $868.13 | $843.07 | $829.13 |

| California | $658.02 | $926.79 | $986.75 | $951.75 | $922.69 | $891.68 | $881.07 |

| Colorado | $638.14 | $898.79 | $981.64 | $939.52 | $887.57 | $849.74 | $835.50 |

| Connecticut | $787.15 | $1,108.67 | $1,151.07 | $1,132.78 | $1,109.03 | $1,082.28 | $1,068.18 |

| Delaware | $842.29 | $1,186.33 | $1,240.57 | $1,215.69 | $1,187.18 | $1,153.59 | $1,134.60 |

| District of Columbia | $928.41 | $1,307.62 | $1,330.73 | $1,324.39 | $1,316.48 | $1,289.49 | $1,276.99 |

| Florida | $856.59 | $1,206.46 | $1,257.13 | $1,208.77 | $1,209.70 | $1,196.57 | $1,160.13 |

| Georgia | $684.94 | $964.70 | $1,048.40 | $991.25 | $949.33 | $922.05 | $912.49 |

| Hawaii | $608.00 | $856.33 | $873.28 | $858.16 | $844.16 | $844.12 | $861.95 |

| Idaho | $466.43 | $656.95 | $679.89 | $673.13 | $650.57 | $639.19 | $641.96 |

| Illinois | $591.74 | $833.44 | $884.56 | $854.10 | $819.27 | $806.21 | $803.04 |

| Indiana | $514.50 | $724.65 | $755.03 | $728.93 | $704.50 | $724.44 | $710.36 |

| Iowa | $477.13 | $672.01 | $702.46 | $683.67 | $668.09 | $656.84 | $648.99 |

| Kansas | $581.59 | $819.14 | $862.93 | $850.79 | $815.82 | $785.72 | $780.43 |

| Kentucky | $642.11 | $904.39 | $938.51 | $917.49 | $904.99 | $888.46 | $872.48 |

| Louisiana | $942.01 | $1,326.78 | $1,405.36 | $1,364.17 | $1,307.72 | $1,275.10 | $1,281.55 |

| Maine | $482.49 | $679.56 | $703.82 | $689.12 | $674.94 | $667.66 | $662.28 |

| Maryland | $765.36 | $1,077.97 | $1,116.45 | $1,096.37 | $1,071.35 | $1,056.82 | $1,048.86 |

| Massachusetts | $763.50 | $1,075.35 | $1,129.29 | $1,107.76 | $1,080.48 | $1,048.06 | $1,011.14 |

| Michigan | $889.11 | $1,252.27 | $1,364.00 | $1,350.58 | $1,264.20 | $1,171.94 | $1,110.64 |

| Minnesota | $586.92 | $826.64 | $875.49 | $856.62 | $823.70 | $800.24 | $777.17 |

| Mississippi | $663.91 | $935.08 | $994.05 | $957.59 | $925.13 | $902.95 | $895.69 |

| Missouri | $586.04 | $825.40 | $872.43 | $845.39 | $819.79 | $799.14 | $790.27 |

| Montana | $598.20 | $842.54 | $863.52 | $868.55 | $842.74 | $821.68 | $816.21 |

| Nebraska | $552.95 | $778.81 | $831.02 | $805.99 | $773.64 | $751.18 | $732.21 |

| Nevada | $750.92 | $1,057.63 | $1,103.05 | $1,083.42 | $1,047.74 | $1,024.09 | $1,029.87 |

| New Hampshire | $552.36 | $777.98 | $818.75 | $795.50 | $773.30 | $755.76 | $746.57 |

| New Jersey | $961.31 | $1,353.96 | $1,382.79 | $1,379.20 | $1,369.70 | $1,334.59 | $1,303.52 |

| New Mexico | $636.57 | $896.58 | $937.59 | $920.42 | $888.83 | $866.19 | $869.85 |

| New York | $923.06 | $1,300.09 | $1,360.66 | $1,327.82 | $1,301.49 | $1,273.70 | $1,236.77 |

| North Carolina | $529.07 | $745.17 | $789.09 | $768.28 | $739.91 | $720.47 | $708.10 |

| North Dakota | $523.72 | $737.63 | $773.30 | $768.09 | $743.27 | $714.75 | $688.74 |

| Ohio | $526.19 | $741.11 | $788.56 | $766.66 | $738.68 | $714.05 | $697.61 |

| Oklahoma | $668.35 | $941.34 | $1,005.32 | $985.58 | $931.41 | $902.90 | $881.50 |

| Oregon | $607.45 | $855.57 | $904.83 | $894.10 | $856.26 | $818.07 | $804.59 |

| Pennsylvania | $663.38 | $934.34 | $970.51 | $950.42 | $930.48 | $915.83 | $904.47 |

| Rhode Island | $865.70 | $1,219.29 | $1,303.50 | $1,257.40 | $1,210.55 | $1,176.05 | $1,148.97 |

| South Carolina | $646.46 | $910.51 | $973.10 | $936.69 | $904.22 | $880.82 | $857.70 |

| South Dakota | $509.59 | $717.73 | $766.91 | $744.28 | $717.30 | $690.95 | $669.20 |

| Tennessee | $584.86 | $823.74 | $871.43 | $855.56 | $829.38 | $794.53 | $767.82 |

| Texas | $728.21 | $1,025.64 | $1,109.66 | $1,066.20 | $1,017.81 | $974.68 | $959.87 |

| Utah | $590.89 | $832.24 | $872.93 | $852.66 | $820.92 | $805.32 | $809.35 |

| Vermont | $523.74 | $737.67 | $764.02 | $746.79 | $734.82 | $726.57 | $716.14 |

| Virginia | $573.47 | $807.71 | $842.67 | $836.14 | $809.40 | $781.38 | $768.95 |

| Washington | $655.44 | $923.16 | $968.80 | $952.10 | $914.04 | $891.04 | $889.82 |

| West Virginia | $721.05 | $1,015.57 | $1,025.78 | $1,032.45 | $1,021.37 | $1,005.68 | $992.57 |

| Wisconsin | $494.24 | $696.11 | $737.18 | $716.83 | $689.77 | $666.79 | $669.99 |

| Wyoming | $579.87 | $816.71 | $847.44 | $844.33 | $804.52 | $796.14 | $791.14 |

| Countrywide | $678.04 | $954.99 | $1,009.38 | $981.77 | $950.92 | $924.45 | $908.43 |

What do I need to know about usage-based car insurance?

Let’s begin by addressing the two main types of usage-based car insurance: pay-as-you-drive car insurance (PAYD) and pay-how-you-drive (PHYD).

Pay-as-you-drive (PAYD) insurance, according to Texas A&M University, “replaces a regular annual automobile insurance payment with one based on mileage actually driven.” Insurance companies incentivize this, the university explains, because “generally, crash rates tend to increase with miles driven and dangerous driving behavior.” This is a great system for people who want to get lower car insurance by driving less.

Pay-how-you-drive (PHYD) insurance, not surprisingly, rewards safe drivers with lower rates. According to the National Association of Insurance Commissioners (NAIC), Pay-how-you-drive programs tend to track not only your lane usage, but also:

- When you drive

- Where you drive

- How fast you drive

- How hard you brake

- How fast you turn

- How quickly you accelerate

In short, usage-based insurance is a quickly growing form of car insurance that can benefit both drivers and car insurance companies. According to MarketWatch:

The global usage-based insurance market is expected to garner $123 billion by 2022, registering a CAGR [compound annual growth rate] of 36.4 percent during the forecast period of 2016–2022. North America is expected to grow at the fastest pace during the forecast period, owing to the upsurge in demand from the U.S. and Canada.

Is UBI the same thing as a low-mileage discount? Read on to find out.

What are other names for usage-based car insurance?

| Insurance Company | Program Name | Earned Savings | Areas Available |

|---|---|---|---|

| Allstate | Drivewise® | 40% | Most states, excluding, CA, DC |

| American Family | KnowYourDrive | 20% | Available in specific states: AZ, CO, GA, ID, IL, IN, IO, KS, MN, MO, NE, NV, ND, OH, OR, SD, UT, WA, WI |

| Farmers | Signal® | 30% | Most states, excluding: AK, HI, LA, MA, MI, NJ, NY |

| Geico | DriveEasy | 25% | Most states, excluding: AK, CA, DC, DE, HI, KS, ME, MA, MO, MS, MT, ND, HD, NY, RI, SD, VT, WV, WY |

| Hartford | TrueLane® | 25% | Most states, excluding: FL |

| Liberty Mutual | RightTrack® | 30% | Most states, excluding: AK, CA, DC, |

| Nationwide | SmartRide® | 40% | Most states, excluding: CA, HI, MA, MI, NY |

| Progressive | Snapshot | 30% | Most states, excluding: DC |

| Safeco | RightTrack® | 30% | Available in specific states, including: FL, IL, MA, MO, RI, NJ, NV, NY |

| State Farm | Drive Safe and Save™ | 30% | Most states, excluding: DC |

| Travelers | IntelliDrive® | 30% | Most states, excluding: CA, HI, NY |

| USAA | SafePilot | 30% | Available in specific states, including: AZ, OH, TX, OK |

If you’re shopping for usage-based insurance, you might hear it called one of the following names: pay-per-mile insurance, black box insurance, pay-as-you-go insurance, UBI, or telematics.

Soon we’ll cover the particulars of the United States’ top car insurance providers’ UBI programs. But for now, it might be handy to know their program titles:

- Allstate – Drivewise

- American Family – KnowYourDrive

- Farmers – Signal

- Geico – DriveEasy

- Liberty Mutual – RightTrack

- Nationwide – SmartRide

- Progressive – Snapshot

- State Farm – Drive Safe & Save

- Travelers – IntelliDrive

- USAA – SafePilot

When you begin to research usage-based car insurance, you’re bound to run into the phrase telematics again and again. So let’s take a look at what that even means.

Free Car Insurance Comparison

Enter your ZIP code below to view companies that have cheap car insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

What is telematics?

Unless you’re an insurance or tech nerd like us, you might not be familiar with the term telematics. But don’t sweat it, we’re here to help you learn.

According to Geotab, telematics is “a method of monitoring an asset (car, truck, heavy equipment, or even ship) by using GPS and onboard diagnostics to record movements on a computerized map.” As we’ve seen above, telematics can track your driving behavior through either a device installed in your vehicle or a smartphone application.

Put more simply, telematics is simply the “long-distance transmission of computerized information,” according to GPS Insight.

But what is telematics even tracking?

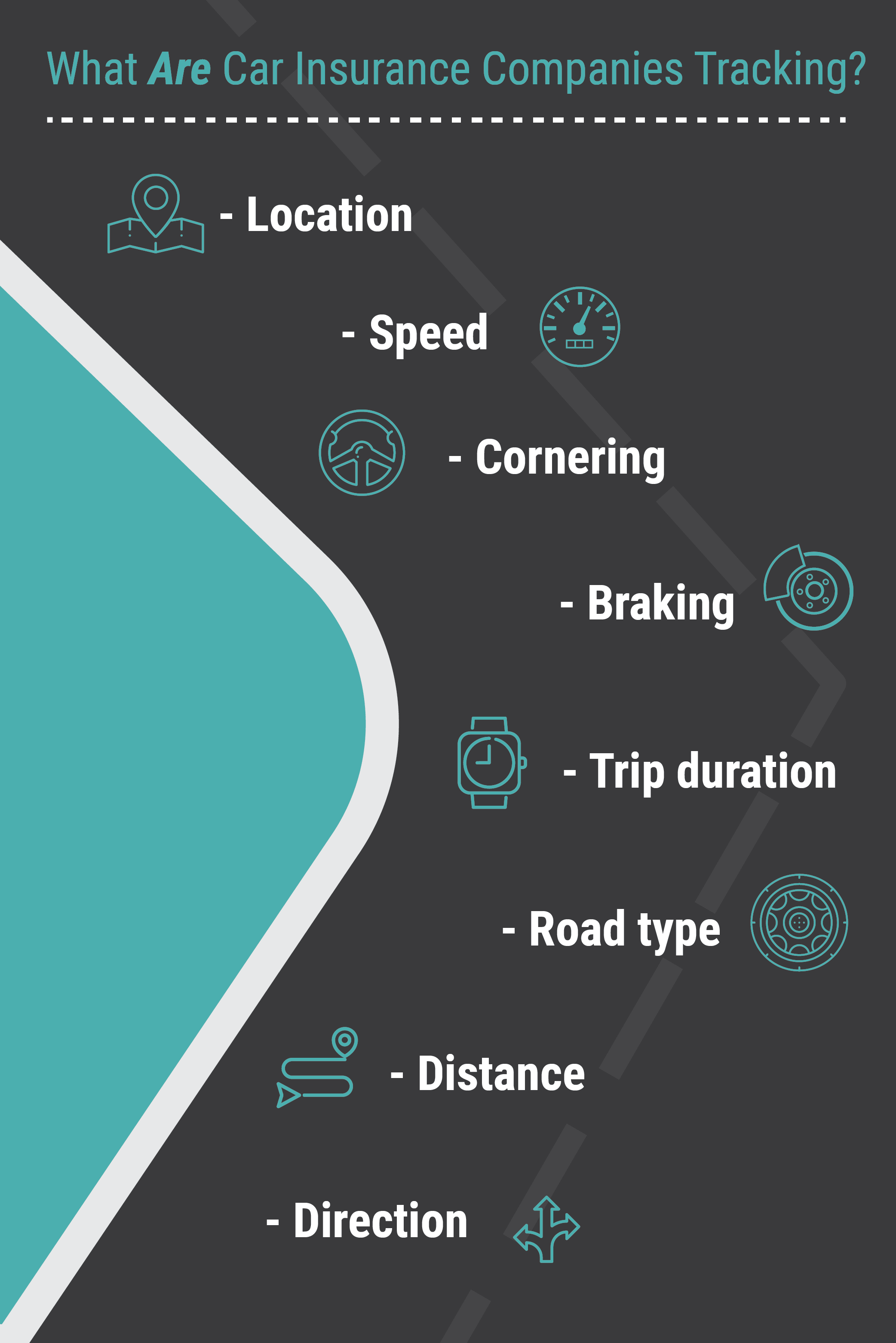

What are car insurance companies tracking?

Car insurance companies use telematics to track a variety of things, including your: location, speed, cornering, braking, trip duration, road type, distance, and direction.

So we’ve talked a bit about telematic devices, but let’s take a deeper dive.

How do insurers collect driving data?

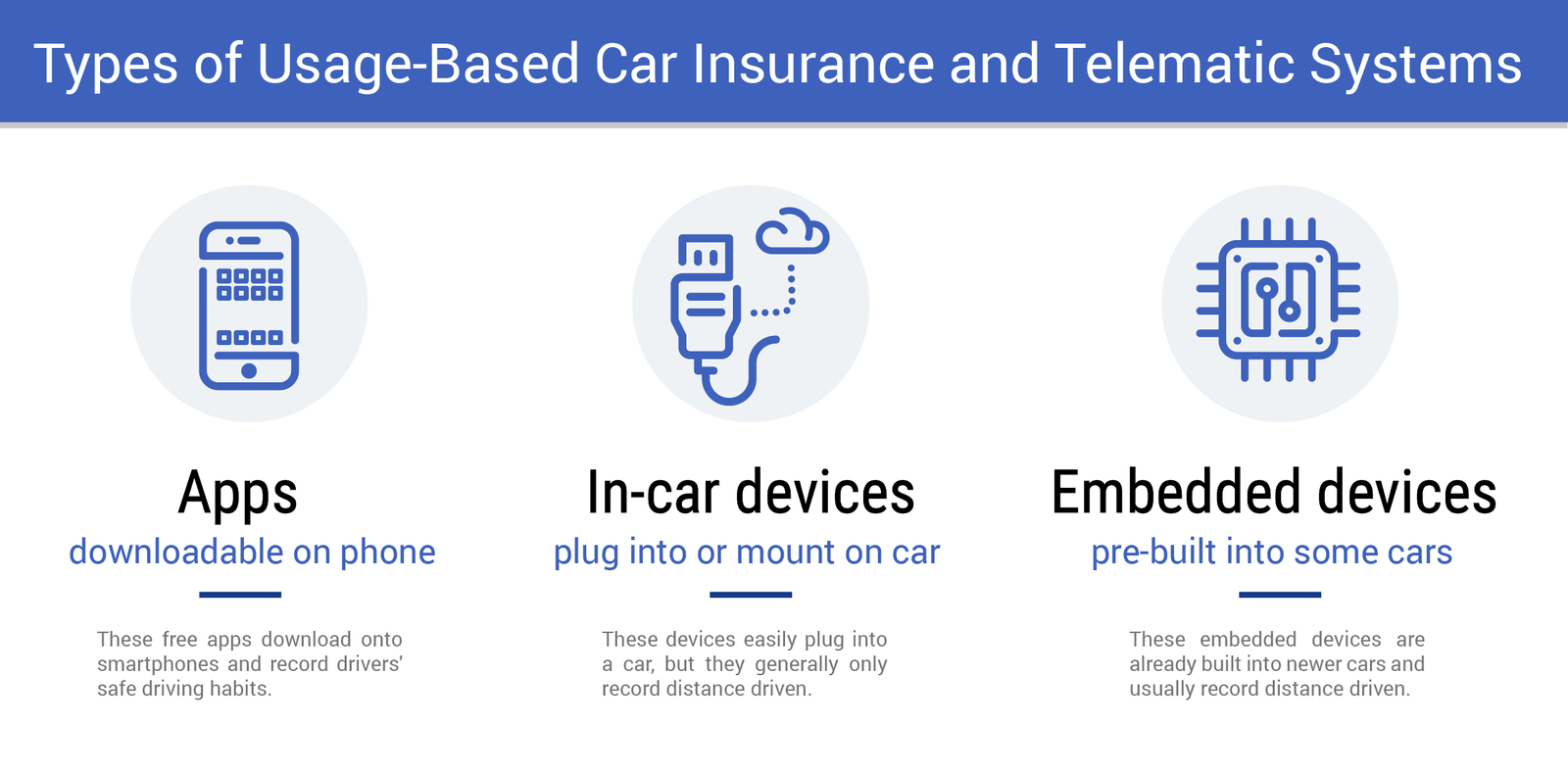

Industry leader IMS reports that car insurance providers primarily use five telematic devices to capture driving data:

- Smartphone/Mobile: A mobile app uses built-in smartphone sensors to detect driving activity. Trip data is collected and transmitted by the smartphone for analysis. It’s best for the following scenarios: driver behavior evaluation, cost-effective regions/markets, try and buy customer acquisition, and low-risk drivers.

- Bluetooth-Enabled Self-Powered Devices: Both Bluetooth-enabled devices are fixed-vehicle devices, paired with a smartphone app to improve trip detection by directly associating the insured vehicle with the collected trip data. It’s best for household vehicle sharing, low-risk drivers, occasional and seasonal vehicles, pre-1996 vehicles, and young drivers.

- Bluetooth-Enabled OBD: This Bluetooth-enabled fixed plug-in device collects driving data which is then transmitted via a smartphone for analysis. It’s best for mileage-based programs, connected car/value-added services, driver fraud concerns, drivers who need high-risk car insurance, and vehicle-centric evaluation.

- OBD: This cellular-based fixed plug-in device collects driving data and transmits directly over cellular networks for analysis. It’s best for mileage-based programs, connected car/value-added services, driver fraud concerns, high-risk drivers, mature drivers/seniors, less technically sophisticated drivers, and vehicle-centric evaluation.

- Black Box: The device is professionally installed in your vehicle and is reliable, flexible and provides “always-on” data stream. It’s best for mileage-based programs, connected car/value-added services, high-fidelity collision detection for emergency services, theft detection and stolen vehicle recovery, driver fraud concerns, high-risk drivers, mature drivers/seniors, less technically sophisticated drivers, and vehicle-centric evaluation.

Your insurance company’s usage-based program may require a specific device, so it’s best to check with your car insurance agent.

Who should use pay-per-mile car insurance?

Auto insurance by the mile is the best car insurance if you don’t drive much. It is also good for people who want more transparency in their car insurance prices and for those who track their mileage religiously.

Others who may benefit from using car insurance by the mile include:

- Students who drive less due to the convenience of living on campus

- Remote workers without a commute

- Those who have additional methods of transportation

- Retirees who no longer drive to work looking for discount car insurance for seniors

Pay-per-mile car insurance allows you to control the amount you pay for coverage, making it an attractive option for those who want more clarity in their auto insurance plans.

Is the use of telematics growing in car insurance?

You might be wondering: Is telematics merely a fad in car insurance, or is it something that will be around for a while? Our research shows that it’s more than just a fad. Telematics is one of the fastest-growing components of the car insurance industry.

The National Association of Insurance Commissioners (NAIC) reports that “by the end of 2018, it’s estimated that 80 percent of new cars for sale in the U.S. will be equipped with onboard telematics devices and by 2020, 70 percent of all auto insurers will use telematics.”

But where is this growth coming from?

What is the history of telematics technology?

According to the Federal Aviation Administration, telematics technology has its roots in GPS, or global positioning system technology.

In March of 1996, they report, President Bill Clinton signed a Presidential Decision Directive on GPS to “encourage acceptance and integration of GPS into peaceful civil, commercial and scientific applications worldwide; and to encourage private sector investment in and use of U.S. GPS technologies and service.”

Soon thereafter, the insurance industry realized it could harness the power of GPS to both protect and serve its consumers. On August 18, 1998, Progressive Insurance published United States Patent US5797134A, becoming the first insurance provider to utilize a motor vehicle monitoring system for determining the cost of insurance.

So where is telematics in usage-based insurance headed?

What is the future of telematics-based car insurance?

Telematics is more than just a fad. When it comes to car insurance, it’s our future, research consistently shows.

According to Global Market Insights, “the global usage-based insurance (UBI) market is expected to grow from its current value of USD 34 billion to over USD 107 billion by 2024.” Or take a look at this Allied Market Research report, where researchers project an annual growth rate of 36.4 percent from 2016 to 2022 for UBI.

While telematics growth has been steady since Progressive took up the technology for insurance purposes first in 1998, growth moving forward is expected to be astronomical.

According to McKinsey & Company, telematics will likely “grow significantly through the first part of the next decade, according to the GSM Association, an organization comprised of mobile-network operators.

“There are two reasons for this. First is the increased willingness of governments to mandate specific telematics services, such as emergency-call capabilities, which is already happening in the European Union and Russia. Second is the increasing appetite from consumers for greater connectivity and intelligence in their vehicles.”

As a car insurance consumer, it’s important for you to have a basic knowledge of telematics technology and usage-based insurance overall, which is why we created this guide. But at this point, you might be wondering: Do telematics help?

Does telematics improve driving?

The short answer is a complicated yes.

According to the Insurance Information Institute (III), “studies indicate crash rates fell between 20 percent and one-third in cars monitored via telematics.”

Telematics is especially helpful in reducing unsafe driving practices in fleet vehicles for fleet car insurance and safety. According to fleet vehicle industry leader Donlen, there are seven specific ways telematics improve fleet driver safety. They report that telematics:

- Track speeding and other unsafe driving habits

- Reduce unnecessary time spent on the roads

- Keep up with the maintenance needs of every vehicle in the fleet

- Respond quickly to emergency situations

- Assign safety training to employees with bad driver behavior

- Reward good driver behavior

- Cut down on fuel costs

Of course, as famed French philosopher Michel Foucault predicted in his book Discipline & Punish, explained in the video below, such technologies train us to regulate ourselves, for better and for worse.

Free Car Insurance Comparison

Enter your ZIP code below to view companies that have cheap car insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

What are the car insurance companies with the best usage-based insurance programs?

| Insurance Company | Program | Device | Enrollment Discount (Up to) | Earned Savings (Up to) |

|---|---|---|---|---|

| AAA | AAADrive | Mobile App | 15% | 30% |

| Allstate | Drivewise | Mobile App | 3% | 15% |

| American Family | KnowYourDrive | Mobile App or Plug-in | 5% | 20% |

| Esurance | DriveSense | Mobile App | 5% | 30% |

| Geico | DriveEasy | Mobile App | - | 20% |

| Liberty Mutual/SafeCo | RightTrack | Mobile App or Plug-in | 5% and up | 30% |

| MetLife | My Journey | Plug-in | 10% | 30% |

| Metromile | Metromile | Mobile App | - | 60% |

| Mile Auto | Mile Auto | Neither | - | 40% |

| Nationwide | SmartRide | Mobile App or Plug-in | 10% | 40% |

| Progressive | Snapshot | Mobile App or Plug-in | average of $25 | 20% |

| State Farm | Drive Safe & Save | Mobile App or Plug-in | 5% | 30% |

| The Hartford | TrueLane | Plug-in | 5% | 25% |

| Travelers | IntelliDrive | Mobile App | 10% | 20% |

| USAA | SafePilot | Mobile App | 5% | 20% |

If by this point you’re interested in usage-based car insurance, we’ve got some good news: the top car insurance companies in the United States all offer comprehensive UBI programs to serve their consumers. And it’s not exactly the same thing as a low-mileage discount as you may have already figured out.

Let’s take a look at each of those company’s UBI programs.

Major Car Insurance Companies With Usage-Based Insurance Programs

In 2008, as we’ve already discussed, leading provider Progressive Insurance took a bold, innovative step: introducing the first wireless telematics device for personal vehicles.

Since then, more and more car insurance companies followed suit, to the point where each of the country’s top 10 providers (in private passenger auto) now offers some form of UBI.

Allstate Drivewise

Since 2010, the Allstate Drivewise program has focused on improving safe driving habits for its consumers.

How to participate:

- Customers and non-customers can begin by downloading the Drivewise app. Drivers who are not customers will be directed to a Drivewise only option.

- Customers opting to use the plug-in device will need to contact their agent to sign up. A device will be mailed to your home, along with instructions.

- You can review your performance on the app, even if you’e using the device.

What’s being tracked:

- Safe speed

- Braking

- Time of day

- Mileage

Potential savings:

- With the device, you can earn up to 10 percent when you sign up, and up to 30 percent every six months for safe driving. For finishing challenges, you can also earn Allstate Rewards Points that can be used toward travel, gift cards, and more.

- With the app, you can earn up to 10 percent cash back for signing up and up to 25 percent cash back every six months for safe driving. You can additionally earn Allstate Rewards Points toward purchases.

American Family KnowYourDrive

Since 2017, the American Family KnowYourDrive program has centered safe driving habits by tracking driving mostly through a mobile app. The company promises that whatever the results of this tracking, your premium will not increase through participation in this program.

How to participate: Customers can enroll by contacting their agent. Drivers will then be directed to download the app, which calculates a driver’s score. This score will be used to determine your discount.

What’s being tracked:

- How often you drive

- Braking

- Acceleration

Potential savings: American Family promises a 5 percent discount for signing up, and up to 20 percent in savings. The lowest discount you can receive is 2 percent.

Farmers Signal

Since 2017, the Farmers Signal program has used an easy mobile app to monitor safe driving habits. This program is not available in all states, and discounts will vary from location to location.

How to participate:

- Contact your agent for a quote and ask to enroll in the program

- Your agent will then text you a link with instructions on how to download the app

What is being tracked:

- Speeding

- Braking

- Distracted driving

- Location

- Mileage

Potential savings: There’s a 5 percent discount for signing up and completing 10 qualifying trips, including up to 15 percent savings at renewal. Additional savings may be possible when multiple drivers on one policy enroll, including those under the age of 25.

Geico DriveEasy

One of the more recent additions to the usage-based insurance scene, since 2019, the Geico DriveEasy program has used the award-winning Geico app to track and score customers’ driving behavior. And some good news: multiple drivers on one policy can participate.

DriveEasy began as a pilot program with a test group in June 2019 under the name Geico Drive. The program has since expanded and is open to all customers. For more information, read our Geico DriveEasy app review.

How to participate: Simply download the DriveEasy app, type in your phone number, and enter the code.

What’s being tracked:

- Speeding

- Braking

- Phone Use

- Time of day

- Distance

Potential savings: Neither Geico’s DriveEasy page nor its FAQs indicate a driver discount for this UBI program. However, with the program still in its infancy, it’s possible discounts could be offered to customers down the road.

Liberty Mutual RightTrack

Beginning in 2016, the Liberty Mutual Insurance RightTrack app-based program has rewarded safe driving with substantial car insurance premium savings.

How to participate: After enrolling in the program (you can do so online or through an agent), download the Liberty Mutual RightTrack app. Your download will trigger the shipment of a device, which needs to be linked to your app. Drive for 90 days to confirm the discount.

What’s being tracked:

- Braking

- Acceleration

- Nighttime driving

- How many miles you drive

Potential savings: Liberty Mutual promises an unspecified discount for signing up, and up to 30 percent savings for the life of your policy.

Nationwide SmartRide

Quick to jump on the telematics UBI market, Nationwide Insurance began Its Nationwide SmartRide program in 2008. The program offers savings for safe driving after four to six months of participation.

How to participate: This program requires the use of a device. Contact your agent to sign up.

What’s being tracked:

- Miles driven

- Hard braking and acceleration

- Idle time

- Nighttime driving

Potential savings: Nationwide promises a 10 percent discount for signing up, and potential savings of up to 40 percent.

Progressive SnapShot

Since 2011, Flo and the folks over at Progressive Insurance have offered the SnapShot program. SnapShot looks at your overall driving habits and mileage and lets multiple drivers on one policy participate easily.

Unlike some other car insurance company’s safe driving programs, you should know that your rates can go up as a result of high-risk driving monitored in the SnapShot program. However, the company claims only two out of 10 drivers see an increase.

How to participate: Drivers can participate with a plug-in device or the mobile app. Where the app isn’t available, customers can use the device. Customers also have the option of enrolling in a 30-day trial.

What’s being tracked:

- Time of day you drive

- Hard braking and rapid acceleration

- The amount you drive

- How you’re using your mobile phone while driving (app users only, in participating states)

Potential savings: An average $26 discount for signing up, and an average discount of $145 savings upon program completion (about six months). Discounts are not available in the following states: Alaska, California, Hawaii, North Carolina, or New York.

https://www.youtube.com/watch?v=Qp1SlGuL6Eo&feature=youtu.be

State Farm Drive Safe & Save

A relative newcomer to the UBI scene, the United States’ largest car insurance provider, State Farm Insurance, began its Drive Safe & Save program in 2019 to offer savings based upon, not surprisingly, safe driving.

How to participate: Drivers can choose to use the app or their vehicle’s OnStar system.

- To download the app and enroll, text SAVE to 78836. Setup will be complete upon the receipt of a Bluetooth beacon sent by State Farm.

- Drivers with OnStar are asked to enroll in OnStar Vehicle Diagnostics (OVD) within 30 days of enrolling in Drive Safe & Save. State Farm will then request odometer information from OnStar within 30 days of you signing up.

What is being tracked:

- Annual mileage

- Braking

- Speed

- Time of day travel

- Acceleration

- Fast cornering

Potential savings: Up to 5 percent for signing up (per vehicle), and up to 50 percent in savings. According to the website: “Your discount is adjusted at each policy renewal (typically every six months). Changes in your driving will be reflected in your discount amount, so your discount amount can increase or decrease at each renewal.”

Travelers IntelliDrive

Since 2017, Travelers Insurance‘s IntelliDrive program has monitored participating customer’s safe driving behaviors. IntelliDrive works by a smartphone app and runs for 90 days.

It’s important to note that IntelliDrive is only available in certain states and that savings can vary by state.

The program is available in Alabama, Arizona, Colorado, Connecticut, the District of Columbia, Florida, Georgia, Iowa, Idaho, Illinois, Indiana, Kansas, Kentucky, Maryland, Maine, Minnesota, Missouri, Mississippi, Montana, Nebraska, New Hampshire, New Jersey, New Mexico, Nevada, Ohio, Oklahoma, Pennsylvania, South Carolina, Tennessee, Texas, Utah, Virginia, Vermont, Washington, and Wisconsin.

How to participate: The IntelliDrive program requires an app and can be used by multiple drivers on one policy. Travelers will send participants a link to download the app.

What’s being tracked:

- Time of day

- Acceleration

- Speed

- Braking

Potential savings: 10 percent for signing up, and potential savings of up to 30 percent at renewal if you’ve driven 13,000 miles or less in a year. Note that riskier driving habits may result in higher premiums, depending on the state you live in.

USAA SafePilot

Beginning in 2019, USAA’s SafePilot began rewarding its members for their safe driving. As the company claims, “The better you drive, the bigger the discount you’ll earn.” It’s important to remember that USAA car insurance is only available to members of the military community and their immediate family members.

How to participate: Participation requires downloading the USAA SafePilot app, available on iOS and Android.

What’s being tracked:

- Phone handling and hands-free phone use

- Braking

Potential savings: Earn 5 percent for enrolling and up to 20 percent at renewal.

Which car insurance companies provide pay-per-mile coverage?

There are different options available for pay-per-mile auto insurance that may work for your budget and needs. Here’s a roundup of popular companies that offer car insurance by the mile.

Metromile

Metromile offers pay-per-mile car insurance, and your bill is divided into two parts: the monthly base rate and a per-mile rate. Because of this, your monthly bill may change depending on how much you drive.

Your base rate is determined by your driving profile. The “Metromile Pulse” device attaches to your odometer and tracks your mileage to determine your rates. The company also offers an app integration that allows you to view your record and monthly bill estimate.

For added value, Metromile comes with a daily cap. After driving 250 miles (150 in New Jersey) in a day, there is no extra charge.

Metromile offers coverage to Arizona, California, Illinois, Oregon, New Jersey, Pennsylvania, Virginia, and Washington residents.

Esurance

Esurance only sells pay-per-mile car insurance to Oregon drivers at this time. For everyone else, it offers an alternative program called DriveSense that includes pay-per-mile options.

Along with being an alternative to insurance by the mile, DriveSense’s main goal is to give personalized discounts based on driving habits. It is similar to pay-as-you-go car insurance in that Esurance calculates your rates based on how many miles you drive, but you can receive additional discounts for safe driving.

Esurance by Allstate pay-per-mile utilizes a mileage tracking device that will monitor your braking habits, acceleration, and deceleration to determine your monthly rate.

It’s important to note that your monthly car insurance rates will not increase for unsafe driving habits, like abrupt braking or accelerating too quickly, but you can receive discounts for keeping these to a minimum.

Nationwide Smartmiles

Nationwide Smartmiles pay-per-mile program is geared toward low-mileage drivers, and rates are a sum of the base rate and rate per mile. It offers a safe driver discount of up to 10%, with an in-car device that counts miles and tracks your driving habits, such as braking, acceleration, speed, and deceleration.

Nationwide Smartmiles is available in 40 states and the District of Columbia. However, unsafe driving habits may be penalized with this plan, which can raise your monthly rates. Consider your driving habits and compare different pay-per-mile insurance companies when deciding which premium will work for you.

Allstate Milewise

Allstate Milewise provides full coverage pay-per-mile car insurance in 21 states. For people who drive less than 13,000 miles a year, it offers valuable savings and additional discount options.

Allstate pay-per-mile uses a daily base rate and mileage rate to calculate your premium, and your miles are tracked via a plug-in device with a mobile app for convenience. Drivers must keep a credit card on file for payment, as charges are assessed after each trip.

Hugo Insurance

Hugo pay-per-mile car insurance calculates your premium by combining a daily and per-mile rate. It doesn’t offer additional discounts but utilizes micropayments and on-demand coverage. These allow drivers to pay for insurance only when they need it and can add to your overall savings.

While their “pay-only-when-you-need-it” insurance model is noteworthy, it can present some potential risks to drivers. For example, turning off your insurance in a public area or while parked could leave your vehicle unprotected from unexpected accidents.

Hugo is a new option on this list, and its coverage options are more limited. Currently, it only offers liability insurance in nine states California, Georgia, Alabama, South Carolina, Florida, Illinois, Ohio, Indiana, and Tennessee.

Mile Auto

Mile Auto offers coverage to Ohio, Arizona, Georgia, Oregon, Illinois, Tennessee, Pennsylvania, Texas, and California. Premiums are calculated with a low base rate and a per-mile rate. They offer additional discounts for safe driving habits, students, and seniors.

Mile Auto allows drivers to send in the number of miles driven at the end of the month by taking a picture of their odometer instead of using a plug-in device.

Noblr by USAA

Noblr assesses your fixed monthly rates based on your primary characteristics, such as age, gender, and driving record. Then it determines the monthly variable rate based on how much you drive and adds it to your total cost.

The Noblr app breaks down your variable write via five characteristics:

- Smoothness

- Focus

- Road choice

- Time of day

- Mileage

This allows drivers to receive a premium that reflects their driving habits, as well as low mileage and encourages transparency.

Noblr provides auto insurance by the mile to Arizona, Ohio, Colorado, and Texas residents and relies on an app to track how much you drive.

What are the downsides to usage-based insurance?

There are certainly some pros to purchasing usage-based car insurance. Most obviously, perhaps, are the potential savings and the ability to live with more frugality and on a better budget.

And we don’t want to downplay the positive change in driving habits usage-based insurance programs are proving to have when people are promised a safe driving insurance discount. A recent study by the Institute for Operations Research and the Management Sciences, for instance, reports that after just six months, UBI users showed a 21 percent decrease in hard braking.

And a survey from the Insurance Research Council shows that 56 percent of its respondents changed their driving behaviors after installing an insurance-issued telematics device in their vehicles.

But did you also know that UBI can result in policies better tailored to your needs and, with some companies, even the option for an expedited and more accurate claims process?

Now let’s dive into some of the cons a little more deeply.

What about privacy concerns?

There’s no other way to say it: privacy matters. And there’s no question that consumers are taking more steps to ensure privacy in all areas, whether that’s in securing the best VPN “or virtual private network” for home internet use, or just being wary about who gets their personal information.

Given the requisite use of telematics and driver tracking technology, there are legitimate privacy concerns when it comes to consumer protections for usage-based insurance policies.

According to the National Association of Insurance Commissioners (NAIC), “a major barrier remains for the public acceptance and the complete mainstreaming of telematics.”

They add that “many consumers have concerns regarding the privacy of the data they share with insurance companies, and they question insurers’ ability to safeguard their data given the recent cases of major corporate security breaches.”

Car insurance companies tout the lower premiums telematics-based insurance can lead to.

But according to the Insurance Journal, “privacy advocates say the lower premiums are not worth the tradeoffs because the data could be used for unexpected purposes like penalizing drivers who visit unsafe neighborhoods. That argument holds sway with the California Department of Insurance, which is opposed to expanding the technology.”

As more and more consumers turn to telematics and usage-based insurance policies, keep a watch out for public conversations around regulatory structures and privacy guarantees for consumers.

Can usage-based car insurance policies distinguish between multiple drivers?

In short: sometimes, but not always.

It depends entirely on the car insurance company’s telematics capabilities. Our research shows that the following companies can distinguish between multiple drivers when tracking driving behaviors:

- Farmers

- Geico

- Progressive

- Travelers

Will telematics work in older vehicles?

Again: sometimes, but not always.

If your car insurance provider uses a mobile app to track your driving behavior and determine your car insurance premium, then you’re probably fine driving an older vehicle.

If your car insurance provider requires the installation of a black box monitoring device, however, some older vehicles might not be capable of holding the technology. Check with your insurance agent if you’re in doubt.

Can my insurance rates actually increase with usage-based car insurance?

A few companies, such as American Family Insurance, guarantee that whatever the results of your driving behavior monitoring, your premium won’t increase.

That’s not always the case, however. A recent University of Connecticut study found that when it came to Progressive Insurance’s SnapShot program, “two out of 10 participants of its UBI program see an increase in their premiums after the discount period ends.”

Two out of 10 drivers might be a vast minority, but it’s worth considering whether your driving behaviors could put you at risk for higher premiums under a usage-based car insurance program.

Free Car Insurance Comparison

Enter your ZIP code below to view companies that have cheap car insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Case Studies: Pay-Per-Mile Car Insurance

Case Study 1: Sarah’s Savings With Low Mileage

Sarah was a low-mileage driver who opted for pay-per-mile car insurance. She drove only 6,000 miles per year, significantly less than the national average. By choosing a pay-per-mile plan, Sarah was able to save money on her car insurance premiums.

Her rates were based on the number of miles she drove, resulting in substantial savings compared to traditional insurance options. This case demonstrates how pay-per-mile insurance can benefit drivers who don’t drive frequently.

Case Study 2: John’s Transparent Pricing

John wanted more transparency in his car insurance pricing and decided to switch to pay-per-mile insurance. He tracked his mileage religiously and wanted a plan that accurately reflected his driving habits. By choosing a pay-per-mile plan, John had full control over his insurance costs.

He paid only for the miles he drove, and his monthly bill accurately reflected his usage. This case highlights how pay-per-mile insurance offers pricing transparency for drivers.

Case Study 3: Laura’s Safe Driving Discount

Laura was a safe driver who wanted to be rewarded for her good driving habits. She switched to a pay-per-mile car insurance plan that offered additional discounts based on safe driving behavior. Her plan tracked various driving metrics such as braking, acceleration, and speed.

By maintaining safe driving habits, Laura received additional discounts on top of the savings she already enjoyed with pay-per-mile insurance. This case demonstrates how pay-per-mile insurance can incentivize safe driving practices.

Usage-Based Car Insurance: The Bottom Line

If you’re a consistently safe driver, or if you don’t drive more than the average American, usage-based insurance may prove to be profitable for you and your family.

You should know, however, that signing up. for usage-based insurance is taking a bet on your driving, and that if that bet doesn’t pay off, your car insurance premiums may actually increase.

Thus it’s important to keep in mind that trackable habits such as hard braking and rapid acceleration will be seen by your car insurance company through the use of telematics.

Of course, none of the potential savings we’ve talked about are possible unless you are willing to consent to be tracked through a telematics device, such as a mobile app or a black box installed in your vehicle. Our research shows that for many, this lack of privacy remains a point of concern.

Bottom line? If you’re still unsure about usage-based insurance, it never hurts to speak to an agent or to pursue programs with car insurance companies that offer trial periods.

Regardless, usage-based insurance is a quickly growing segment of the car insurance industry, and we hope this guide has helped you learn more about it.

What part was the most helpful? Is there something we could explain more clearly?

Use our FREE quote tool below to get started on your car insurance journey today simply by entering your ZIP code.

Frequently Asked Questions

Can usage-based car insurance save me money?

Yes, if you’re a safe driver with low mileage, it can potentially lower your premiums.

Do I need a specific vehicle for usage-based car insurance?

Usage-based car insurance is typically available for a wide range of vehicles.

Can I switch back to traditional car insurance after using usage-based car insurance?

In most cases, you can switch back to a traditional policy.

Are there additional benefits to using usage-based car insurance?

Yes, such as personalized feedback, access to driving data, and vehicle tracking.

Are there restrictions on when and where I can drive with usage-based car insurance?

Generally, there are no driving restrictions, but there may be specific programs or discounts for off-peak hours or limited distances.

Can usage-based car insurance help inexperienced or young drivers?

Yes, it can help them improve driving skills and potentially lower premiums based on driving performance.

Does pay-per-mile auto insurance include full coverage car insurance?

Full coverage car insurance generally includes liability, collision, and comprehensive insurance. These coverage options are available with pay-per-mile plans from some companies, so compare different insurers to find the best one.

Can I get car insurance discounts with pay-per-mile auto insurance?

Some insurance companies will offer a discount based on a mileage threshold. For example, if the threshold is 10,000 miles, and you drive less than that, your insurance company may provide a discount on your monthly rates.

You may also receive safety discounts, like with Nationwide SmartMiles and Metromile. For these discounts, the mileage counter you receive will also track your driving habits, such as sharp turns or abrupt braking, to determine if you are practicing safe driving.

How do insurance companies check mileage?

There are two main ways that insurance companies check mileage. The first is through a device that drivers attach to their vehicles. This device will count their miles and track their driving habits for potential safety discounts.

The other option is for you to take a picture of your mileage counter each month and submit it to the company to get your rates. Many insurance companies offer an app integration to view mileage as well.

Which car insurance companies provide pay-per-mile coverage?

There are several car insurance companies that offer pay-per-mile coverage. Some popular options include Metromile, Esurance, Nationwide Smartmiles, Allstate Milewise, Hugo Insurance, Mile Auto, and Noblr by USAA. Each company has its own pricing structure and coverage options, so it’s important to compare quotes and find the one that suits your needs.

What should I consider when choosing car insurance by mileage?

When choosing car insurance by mileage, it’s important to consider factors such as your actual mileage, the cost per mile, and any additional discounts or benefits offered by the insurance company. You should also ensure that the insurance company provides the coverage you need, whether it’s liability, collision, or comprehensive insurance.

Free Car Insurance Comparison

Enter your ZIP code below to view companies that have cheap car insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Brandon Frady

Licensed Insurance Agent

Brandon Frady has been a licensed insurance agent and insurance office manager since 2018. He has experience in ventures from retail to finance, working positions from cashier to management, but it wasn’t until Brandon started working in the insurance industry that he truly felt at home in his career. In his day-to-day interactions, he aims to live out his business philosophy in how he treats hi...

Licensed Insurance Agent

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.